Following the flurry of technical announcements earlier this week, the second week of March 2026 has shifted the focus toward industrial execution. We are moving past the “wow factor” of a five-minute charge and into the gritty reality of scaling these systems for global fleets. For the C-suite, the takeaway is clear: the technology is no longer a bottleneck; the challenge is now manufacturing velocity and software integration.

The conversation is no longer about “if” these batteries work, but about how quickly they can be integrated into your 2027 product roadmap.

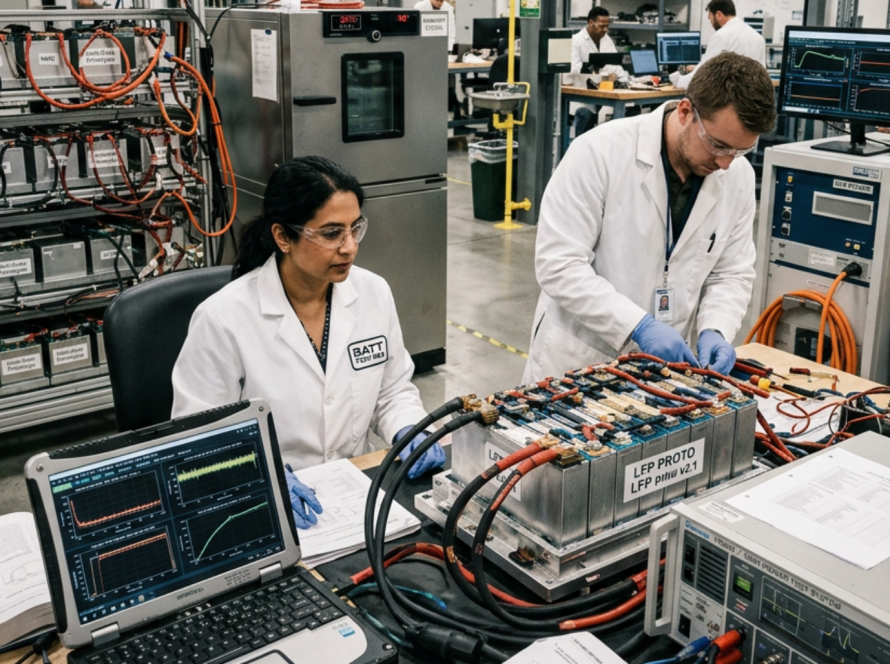

From Prototypes to “A-Samples”

The most significant operational update this week involves the transition of solid-state technology from Nankai University’s labs to “A-Sample” validation for major OEMs.

- The Milestone: Several Tier-1 suppliers in East Asia have confirmed they are now delivering 500 Wh/kg solid-state samples to European and North American automakers for rigorous winter testing.

- The Impact: This signifies that the chemistry is stable enough for automotive-grade environments. For executives, this is the signal to begin finalizing vehicle architectures that can accommodate these higher energy densities without the traditional weight penalties of liquid-electrolyte packs.

AI-Integrated Battery Management: The “Digital Cell”

While the hardware is scaling, the software layer is becoming the true competitive differentiator. Samsung SDI’s “AI-Battery” vision, showcased this week, represents a move toward predictive cell health.

- Real-Time Optimization: By embedding AI directly into the Battery Management System (BMS), 2026-model vehicles can now adjust their charging curves in real-time based on ambient temperature and historical usage patterns.

- Extended Lifecycles: These AI-driven systems are projecting a 20% increase in total cycle life, effectively turning a ten-year battery into a fifteen-year asset. This dramatically changes the residual value calculations for leasing and fleet management companies.

The Sodium-Ion “Mass Market” Reality

While solid-state targets the premium segment, sodium-ion is officially claiming the entry-level market. As Natron Energy scales its Michigan operations, the first commercial-grade sodium-ion packs are being integrated into stationary storage and urban micro-mobility.

- Supply Chain Resilience: Because sodium is abundant and geography-neutral, this week’s rollout provides a critical hedge against the volatility of the lithium carbonate market.

- Economic Parity: In the $25,000 EV segment, sodium-ion is now providing a 15-20% cost advantage over traditional LFP, allowing manufacturers to maintain margins while meeting aggressive price targets.

Strategic Hurdles for the C-Suite

As these “Next-Gen” batteries move toward the assembly line, leadership teams must manage three primary complexities:

- Thermal Management Synchronization: The ultra-fast charging of the Blade 2.0 and solid-state cells generates significant heat. Your facility’s charging infrastructure must be synchronized with the vehicle’s active cooling software to prevent “thermal throttling.”

- Chemistry-Agnostic Logistics: Distribution and service centers must be equipped to handle multiple battery types (LFP, Sodium, Solid-State), each requiring specific safety protocols and recycling pathways.

- The Interconnection Queue: Scaling 1.5 MW charging stations isn’t just a hardware purchase; it’s a grid-negotiation task. Securing high-voltage permits is now the longest lead-time item in any EV rollout strategy.

The Bottom Line

The narrative has shifted from “lab breakthroughs” to industrial asset management. With AI-managed cells and the commercial arrival of 1,000 km ranges, the battery is no longer a mystery box—it’s a programmable component of your infrastructure. The 2026 winners will be those who stop waiting for the “perfect” chemistry and start building the software-defined platforms that can manage all of them.